Can I Put Money From My Savings Account Into A Roth

The Thrift Savings Programme (TSP) was created nether the Federal Employee's Retirement System Act of 1986 for federal employees and members of the uniformed services. This is an Employer-sponsored retirement account that allows participants, Federal Employees, to participate in a low-cost investment and receive an employer match on some of their contributions.

Federal Employees enrolled in the TSP have two "buckets" within their TSP account.

Pre-Tax Account: The first "bucket" is the Traditional element. This allows you to make contributions on a taxation-deferred footing. When nosotros defer taxes, that ways that we are putting them off until later.

The money that you put into the Traditional TSP is washed so on a pre-tax ground. When you withdrawal those funds later at a qualifying historic period, they are considered taxable income.

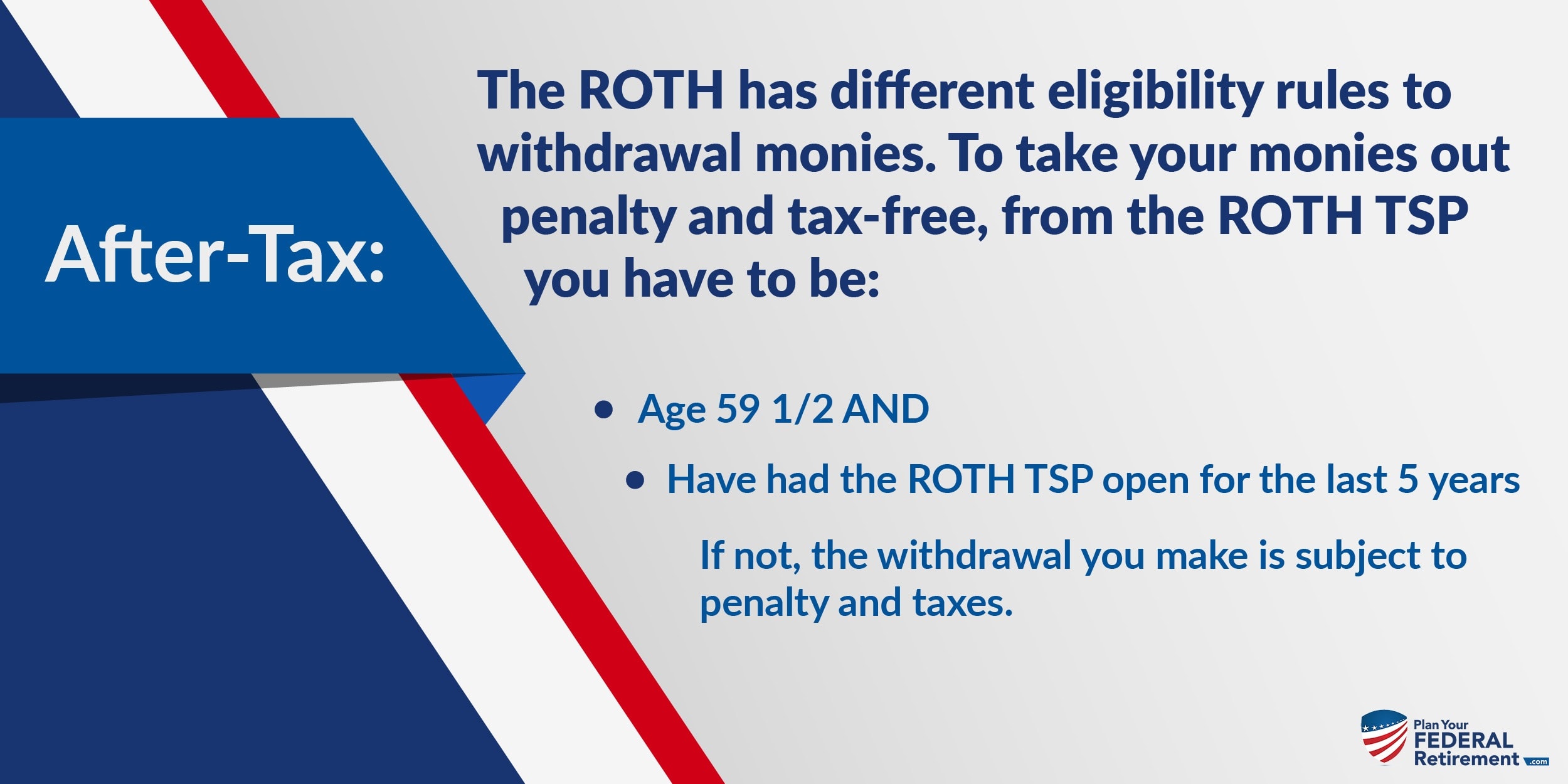

After-Tax Business relationship: The after-tax account is called the "ROTH" TSP. This account was named after Senator Roth who helped laissez passer the legislation assuasive monies invested to be made on an after-taxation basis to this business relationship.

When you make a contribution to the After-Tax account of your TSP, the ROTH, your funds grow tax-free. You already paid taxes when you made the contribution so when y'all go to withdraw those funds, once yous come across eligibility requirements, they are tax-free.

Accessing Pre and Post Tax Contributions to the TSP

The Pre-Taxation and After-Tax accounts have unlike rules as to when yous can access those funds.

In the private sector, people participate in Private Retirement Accounts (IRA's) which accept an age requirement that y'all reach 59 1/2 before yous tin can withdrawal your monies from an IRA without penalty.

The TSP, for Federal Employees, is different. Here is how:

However, whatsoever monies yous take out of this account are discipline to income taxes. This account was fabricated on a pre-tax basis so when y'all withdraw those funds, taxes are owed at your ordinary income taxation rate.

Employer Contributions

Employer contributions to the TSP are ever made to the Pre-Tax Account.

Even if 100% of your contributions are made to the ROTH TSP, your Employer's contributions will be made to the Pre-Tax TSP account.

How Much Can You Contribute to the ROTH TSP?

Every twelvemonth the Internal Revenue Services establishes the maximum contribution levels that Employees can contribute to their employer plans.

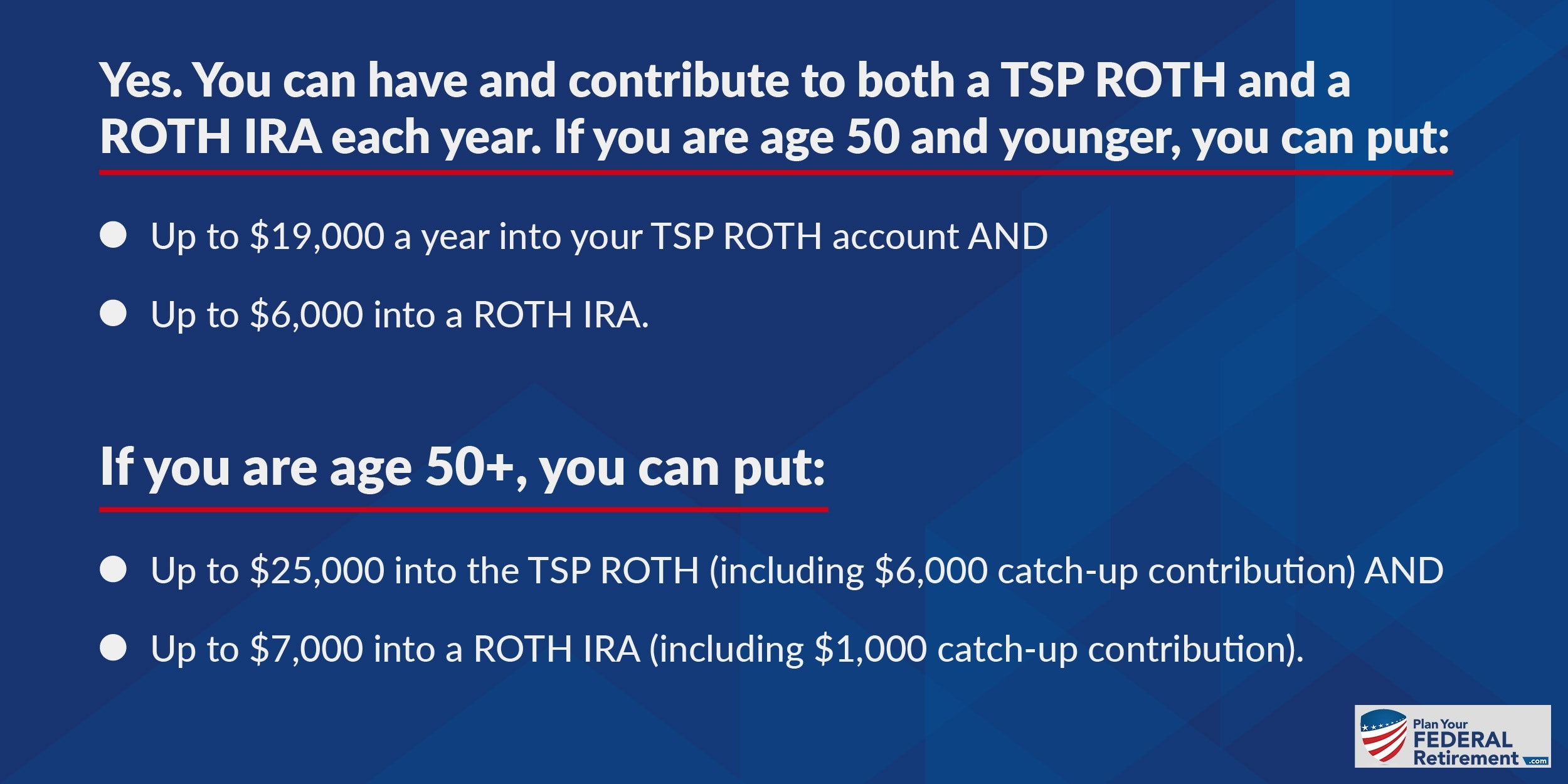

In 2019, the maximum contribution that a Federal Employee can make to their TSP account is $19,000 if they are younger than historic period 50.

If they are older than age 50, they can make a $19,000 contribution and elect to brand a "catch-up" contribution of $6,000 additionally. This is a full of $25,000 that tin exist contributed to the TSP if y'all are historic period 50+.

Each twelvemonth the IRS reassess this amount and publishes new guidelines as to what the annual contribution limits are. Changes, from twelvemonth to year, are generally around $500.00.

Can I Accept a ROTH TSP and a ROTH IRA?

Think, with an IRA, ROTH IRA, and TSP ROTH you accept to reach age 59 ane/2 before you lot tin can withdraw those funds without penalty. Also, with the ROTH IRA and TSP ROTH, you have to take had the business relationship open for longer than five years.

Are there income limits to the ROTH?

The TSP ROTH is not subjected to income limitations for participants. You tin contribute to the TSP ROTH even if you are a high-income earner without a stage out qualifications.

However, the ROTH IRA is subject field to income limitations. If the adapted gross income for your household exceeds $180,000 a year, y'all volition want to talk with a financial professional. They can see if a "dorsum door ROTH IRA" potentially makes financial sense for you.

Source: https://plan-your-federal-retirement.com/can-you-have-a-roth-tsp-and-a-roth-ira/

Posted by: trujilloanswert.blogspot.com

0 Response to "Can I Put Money From My Savings Account Into A Roth"

Post a Comment